Mastering Your Finances: Expert Tips and Strategies for Financial Success

Getting on top of your finances and expenses is critical to ensuring that you can maximize the money you make and achieve the lifestyle that you desire. A big part of mastering your finances includes learning how to live within your means, save for a rainy day, and still have enough left over to do something fun now and again. Read on to discover eight things you can do to master your finances.

How to master your finances

Mastering your finances requires some time, patience, and perseverance. By following these eight tips, you’ll not only be on your way to a better way of life, but you’ll also be able to improve your credit score while embracing life long skills that will help you in more ways than you can imagine.

1. Adopt a budgeting methodology

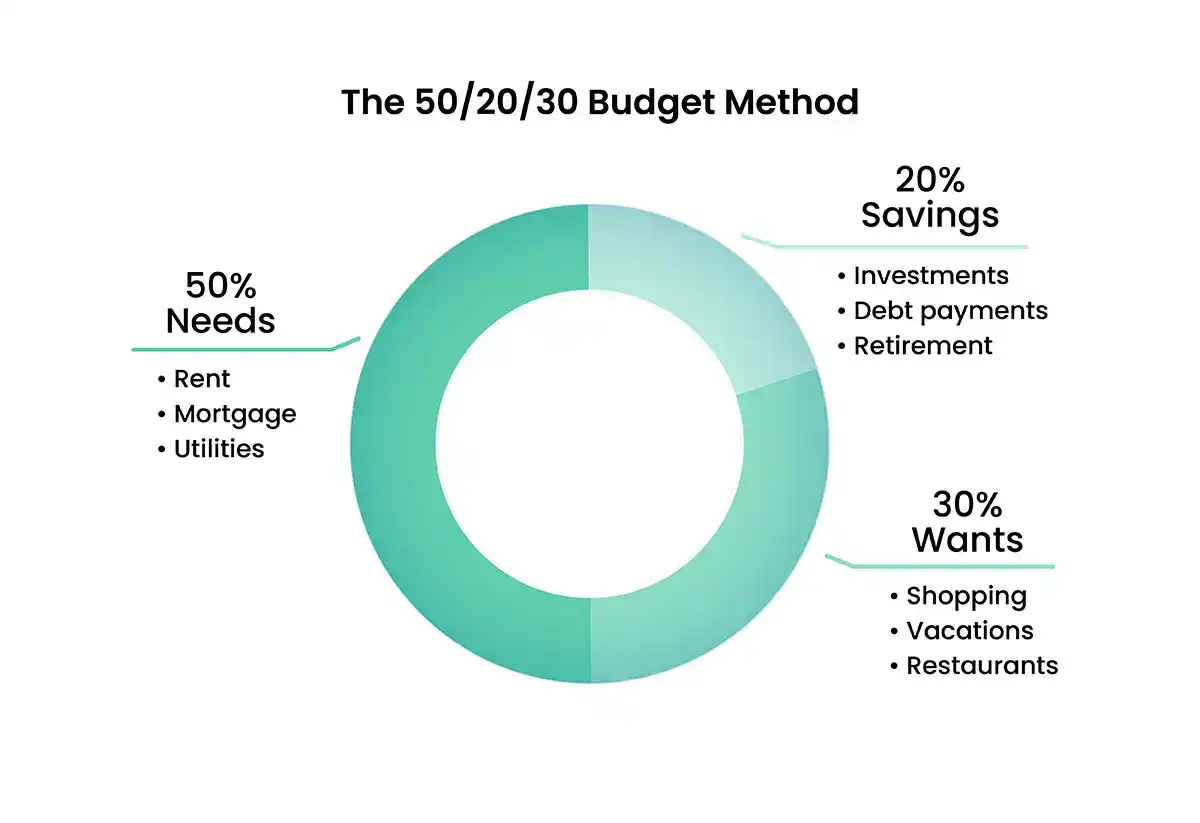

There are many ways to tackle your monthly or household budget, but one of the most tried-and-true strategies is the 50/20/30 methodology. With this approach, you divide your income into three categories. 50% of your money should go towards needs, 20% to savings, and 30% to wants.

Your needs include housing expenses (rent, mortgage, or utilities). Your wants are things like that pair of designer jeans you’ve been eyeing, or even your dream family vacation to Disney World. Finally, your savings could be your investments, savings account, or 401(k).

2. Pay with cash vs. credit

Another great way to stay on top of your finances and your new budget is to pay with cash whenever possible. It is so easy to get carried away with credit card bills. Before you know it, you might have spent over 30% of your credit card limit, creating a dent in your credit score. You never want to risk spending so much that you can’t manage your monthly payments. Paying with cash helps ensure you avoid spending more than 30% on your wants.

3. Educate yourself on the concepts of personal finance

Readily available new sources are a luxury in our modern world. You may already read the newspaper, watch the news sites, get information from Facebook, or turn on the local news at 10 PM each night. Modify this habit to create space for educating yourself about personal finance regularly. Dip into an article from the Cash Store blog occasionally, read articles from Kiplinger, or listen to a podcast like NPR's Planet Money while on your way to work. Before you know it you’ll be up to date on all things finance.

4. Begin saving for your retirement

If your employer offers a 401(k) program and you have yet to begin participating, there is no time like the present to start. Putting money in your 401(k) not only helps you save for retirement, but because the money is deducted from your paycheck before taxes are taken out, you end up paying less in taxes on your salary. If your employer does not offer a 401(k) plan, try an IRA, brokerage, or Solo 401(K) account. Any reputable investment firm can help.

5. Set aside some money for emergencies

The sad truth is that emergencies happen; by definition, they aren't something you can plan for. As part of your 50/20/30 budgeting plan, 20% of your savings should go towards emergency funds, retirement, and a savings account. While the amount you put towards your 401(k), your savings account, and your emergency fund is ultimately up to you, we recommend that you aim to have at least three to six months' worth of expenses dedicated just towards an emergency fund. Try and make sure it’s a separate savings account that isn't used to fund your wants.

6. Be mindful about your taxes

As Americans, taxes are inevitable each year. If you aren't careful with your deductions, you could have to pay quite a bit at the end of the year. Whether you are self-employed or work for an employer that helps you manage your taxes, understanding the federal tax brackets is an excellent way to ensure you stay mindful of what you will have to pay so you don't end up with an unpleasant surprise come tax season.

7. Enroll in the best health insurance plans available to you

Since 2015 as part of the federal Affordable Care Act (ACA), employers with at least 50 employees need to offer group health insurance to full time workers. Paying a monthly premium for your health and dental insurance might seem expensive, but this premium and any co-pay our remaining out-of-pocket expenses will be far less than what you would have to pay for a medical emergency without insurance. Take this example: the out-of-pocket cost for a broken leg without medical insurance could easily cost $18,000 or more.

8. Live within your means

The 50/20/30 budgeting methodology is rooted in living within your means. Spending time actually learning how to live within your means takes time, patience and practice. The goal is to set realistic parameters around what you do daily, and understand your costs of daily living. When making financial decisions, such as purchasing a new home, a car, or even a new wardrobe, think about the impact of the purchase and the opportunity cost.

Let’s think big. Say you want to buy a home; it’s an exciting move. But before signing that dotted line, have you thought about the whole picture? What percentage of your income would a new mortgage consume? Will you have to cut things out of your daily living to afford this new cost? Will you still have the space to commit to sending cash to your savings account each month? In taking the time to really think through these questions, you will actually be able to feel the joy that comes with making big purchases! Our advice - mitigate stress by mapping out the full picture. Take the time to make the right decision, and set yourself up to enjoy all the benefits that come with it.

Mastering your finances is all about time, patience, and perseverance

Mastering your finances takes time, patience, and perseverance. But once you have learned the 50/20/30 budget and have gained an awareness about financial responsibility, you'll be better equipped to stay on top of balancing and budgeting for your wants, savings, and needs. You will also improve your credit score due to your good financial decisions, making you eligible for things like installment loans and other financial products that can help you attain your goals.

*The content on this page provides general consumer information or tips. It is not financial advice or guidance. Each person’s circumstances are unique. The Cash Store may update this information periodically. This information may also include links or references to third-party resources or content. We do not endorse the third-party or guarantee the accuracy of this third-party information. There may be other resources that also serve your needs.

More Articles

Installment vs. Revolving Loans: What’s the Difference?

Wondering about the difference between installment vs revolving loans? Learn about these different common loan types and which structure is right for your financial needs.

Read More >Things to Know When Applying For a Credit Card

Thinking about applying for a credit card? Learn how credit card applications work, the fees and terms involved, and what to ask about to make sure you are fully informed.

Read More >Tips to Manage Money During Unemployment

Unemployment can be stressful and challenging for anyone. Here are some tips for managing your money during unemployment to weather the storm until your next job.

Read More >

Loan Amount is subject to loan approval. Loan terms and availability may vary by location. Approval rate based on complete applications received across all Cash Store locations. Customers can typically expect to receive loan proceeds in less than 20 minutes; however, processing times may vary. Loans / Advances are provided based on approved credit. Each applicant for credit is evaluated for creditworthiness. Vehicle is subject to evaluation for title/auto equity loans.

Please see the Licenses and Rates page for additional product details.

Cottonwood Financial offers consumer credit products that are generally short-term in nature and not intended for long-term borrowing needs.

In Texas, Cash Store is a Credit Services Organization and Credit Access Business. Loans are provided by a non-affiliated third-party lender. Please see the Licenses and Rates page for links to Consumer Disclosures and choose the one for the product and amount that most closely relates to your loan request.

Customer Portal residency restrictions apply. Availability of funds may vary by financial institution.