Is Your Retirement Savings Where it Needs to Be?

Retirement savings, an often underestimated aspect of financial planning, have never been more critical. According to a 2023 Fidelity report, the average American has saved just 78% of what they'll need for retirement, and a startling 52% of U.S. households may struggle to cover essential expenses during their golden years.

These concerning statistics reflect the evolving financial landscape where real income is declining while real spending is on the rise. As if this weren't challenging enough, interest rates are at an all-time high, with the average 30-year fixed rate at 7% during the third quarter of 2023 and expected to rise slightly to 7.1% by year-end, as forecasted by Fannie Mae. In fact, it's not expected to dip below 6% until 2025.

This means that now, more than ever, understanding where you stand regarding retirement savings is crucial.

How Do You Compare? Average Retirement Savings by Age Revealed

In this article, we'll explore the world of retirement savings, shedding light on the savings habits of different age groups. We'll look at not only how much you should ideally be setting aside for your golden years but also offer strategies to boost your retirement savings if you find yourself falling short. Your financial future is at stake, and it's time to take control.

The Importance of Comparing Your Savings

Why should you compare your retirement savings? The answer lies in the financial security of your future. Starting early can make all the difference. By assessing your savings, you can ensure your family budget aligns with your wealth planning goals.

One effective budgeting system is the 50/20/30 rule. This suggests allocating 50% of your income to essentials, 20% to savings and debt reduction, and 30% to personal expenses. When it comes to retirement savings, this means allocating a substantial portion of your income to secure your future.

As a rule of thumb, by age 30, you should aim to have at least one times your annual salary saved. For instance, if you earn $50,000 a year, your goal should be to have $50,000 saved for retirement. As you progress, the milestones become more substantial. By age 40, target three times your annual salary saved, and by age 50, the goal is to have six times your salary securely set aside. These benchmarks can guide your retirement planning and help ensure a comfortable and worry-free retirement.

Average Retirement Savings by Age

Understanding savings by age is crucial for effective retirement planning. We'll break down the average retirement savings by age groups to help you gauge where you stand and provide valuable insights for your financial future.

Whether you're just starting out or approaching retirement, knowing how your savings compare is a significant step towards securing your golden years.

20s-30s: The Starting Point

In your 20s and 30s, you're at the beginning of your journey towards a secure retirement. Fidelity suggests that a person should aim to save at least 1 times their income by age 30. Their approach factors in a consistent 15% (or 20% based on the 15/20/30 plan) annual savings from age 25, with more than 50% of savings invested in stocks over a lifetime.

Achieving a goal of 10 times your pre-retirement income by age 67 may seem ambitious, but with diligent saving, you can build the foundation for a comfortable retirement.

40s: The Midway Check

As you hit your 40s, it's time for a mid-course evaluation. Fidelity recommends targeting 3 times your income by age 40. For instance, if you earn $60,000 annually, your savings goal should be around $180,000.

This milestone signifies substantial progress toward your ultimate retirement savings goal, ensuring you're on track to enjoy a comfortable retirement.

50s: The Critical Decade

In your 50s, you're in the critical decade of retirement planning. Fidelity advises having 6 times your income saved by age 50. If you earn $60,000 a year, this means aiming for a nest egg of $360,000. At this stage, compound interest plays a pivotal role.

Every dollar saved not only grows but also begins to work for you, helping you bridge the gap towards a financially secure retirement. It's a decade where your savings can significantly benefit from the magic of compounding.

60s and Beyond: The Home Stretch

In your 60s, you're approaching the finish line of your working years. Fidelity recommends having 8 times your income saved by age 60. So, if your annual income is $60,000, your target would be $480,000.

As you near retirement, this milestone is crucial to ensure that your golden years are truly golden. It's your last opportunity to boost your savings, secure your financial future, and enjoy the retirement you've always dreamed of.

Factors Affecting Retirement Savings

Your retirement savings journey is influenced by several key factors. These include your income levels at various stages of life, the investment choices you make, unexpected financial setbacks such as unemployment, and even your overall financial health.

Understanding these factors can help you make informed decisions and adapt your savings strategy to navigate the complexities of modern retirement planning.

Income Levels

Your income levels throughout your working years have a significant impact on your retirement savings. Experts recommend aiming for an income replacement rate of at least 75% during retirement.

This means that your retirement savings should be able to replace 75% of your pre-retirement income to maintain your current lifestyle. Therefore, it's crucial to consider your earnings trajectory and adjust your savings strategy accordingly to ensure financial security in retirement.

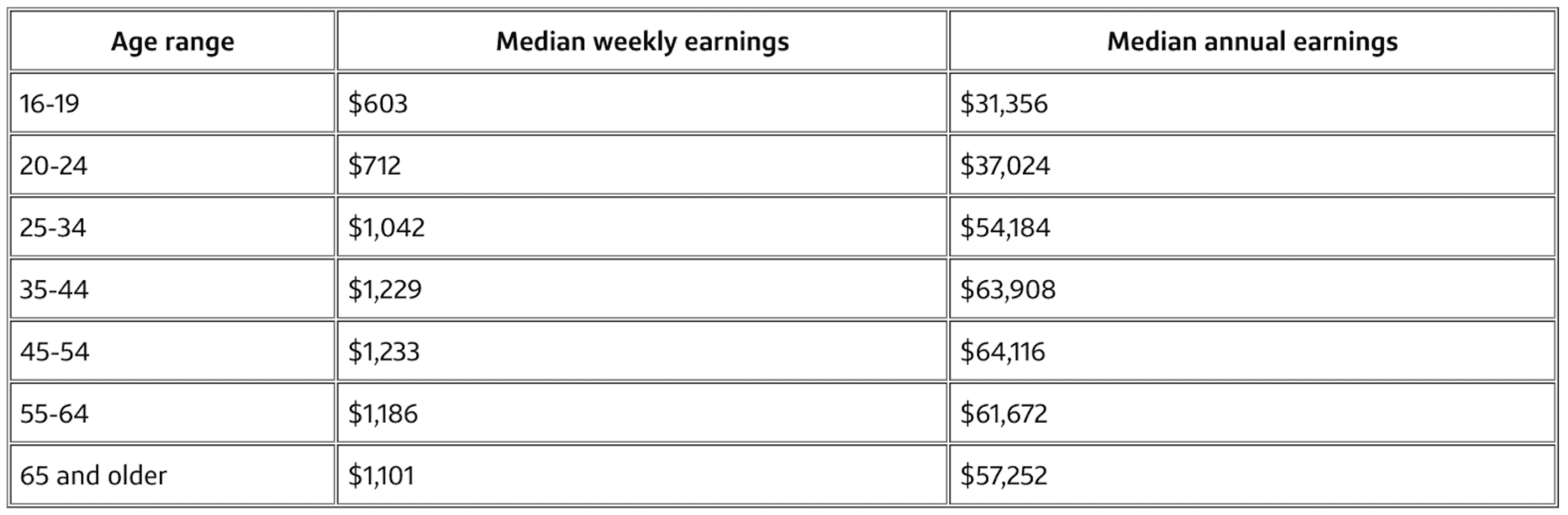

Average Income by Age

You might not be aware, but the U.S. Department of Labor’s Bureau of Labor Statistics (BLS) meticulously monitors national employment data, including income levels. In the chart below, you can observe the median salaries for full-time wage and salary workers aged 16 and older during the second quarter of 2023, as reported by the BLS.

Median income is a statistical measure where half of the incomes fall below the median, and the other half are above it. It provides a more accurate representation of typical earnings, making it a valuable reference for assessing how your income aligns with your peers in your age group. Understanding the median income by age can help you gauge where you stand in terms of your earning potential and how it may influence your retirement savings.

How income relates to savings

Recently, the savings rate in the United States seems to be on a downward trend. In May 2023, it stood at 5.3%, but by August 2023, it had dropped to 3.9%. This fluctuation raises questions about the relationship between income and savings.

Looking back, in the 1970s and 1980s, personal savings rates were consistently in the 7% to 15% range. However, early in the 21st century, they plummeted to a concerning low of 2.1% in 2005. This shift reflected a time when many Americans struggled to save.

It's crucial to understand that income and savings are interlinked but don't always move in harmony. While higher income often allows for more savings, personal financial habits, economic conditions, and debt levels also play a significant role. The increase in savings after the 2008 financial crisis is an example of how economic conditions can influence saving behaviors.

The declining savings rate, despite income growth in some cases, serves as a reminder that building a solid financial future involves prudent financial decisions, irrespective of your income level.

Investment Choices

Your investment choices play a pivotal role in your retirement savings journey. They can significantly impact the growth of your nest egg. It's important to understand the risk levels associated with different options. Here are some common investment choices:

- Stocks: High risk, potentially high return.

- Bonds: Moderate risk, steady returns.

- Real Estate: Moderate to high risk, potentially high returns.

- Mutual Funds: Diversified portfolios, moderate risk.

- Savings Accounts/CDs: Low risk, low return.

- Retirement Accounts (e.g., 401(k)): Varies based on investments selected.

Diversifying your investments can help manage risk while optimizing potential returns for your retirement savings.

The role of 401(k)s and IRAs

401(k)s and IRAs (Individual Retirement Accounts) are essential tools in your retirement savings arsenal, but they differ in significant ways.

- 401(k): These are employer-sponsored retirement plans. Contributions are deducted directly from your paycheck, and often employers match a portion of your contributions, which is essentially free money. The funds are invested in a variety of options, typically stocks and bonds.

- IRA: IRAs are individual accounts you set up independently. They come in two main types, Traditional and Roth. Traditional IRAs offer potential tax benefits when you contribute, while Roth IRAs offer tax advantages when you withdraw funds.

The key difference is in how contributions and withdrawals are taxed. 401(k)s and Traditional IRAs offer tax deductions on contributions, but withdrawals are taxed. Roth IRAs, on the other hand, provide no tax deductions on contributions but offer tax-free withdrawals.

The amount you will have for retirement depends on how much you contribute, the investment choices you make within these accounts, and the tax treatment. Utilizing both 401(k)s and IRAs effectively can significantly boost your retirement savings.

Understanding risk and reward

Imagine you have $10,000 to invest for retirement:

- High Risk, High Reward: You could choose to invest in individual stocks. There's a chance for significant gains, but also the risk of substantial losses. Your $10,000 might double or triple, but it could also shrink.

- Moderate Risk, Steady Returns: Opting for bonds or bond funds might offer a safer path. Your $10,000 may grow steadily, providing a dependable income source during retirement, but the returns are usually more modest.

- Balanced Approach: A mix of stocks and bonds can offer a compromise. This balances the potential for growth with stability, making it suitable for many retirement portfolios.

Your risk tolerance, time horizon, and financial objectives should guide your investment choices. Diversification across various assets can help you strike the right balance between risk and potential rewards in your retirement savings portfolio.

How to Boost Your Retirement Savings

Boosting your retirement savings doesn't have to mean sacrificing your current lifestyle.

Consider these strategies to boost your retirement savings:

- Save 1% more of your income.

- Redirect pay raises and bonuses into your retirement accounts.

- Contribute your tax refunds.

- Allocate unexpected windfalls toward retirement.

- Maximize your 401(k) match.

- Utilize available tax breaks.

- Reduce investment fees.

- Avoid early withdrawal penalties.

- Trim one unnecessary expense.

- Automate savings to make consistent contributions painless.

Start Early and Invest Consistently

The power of starting early and maintaining a consistent investment strategy cannot be overstated. The longer your money has to grow, the more it can benefit from compounding, which magnifies your returns over time.

By consistently investing a portion of your income and working towards that 20% goal for savings, you'll build a robust retirement nest egg that can weather market fluctuations and secure your financial future.

Take Advantage of Employer Matches

Employer matches in retirement accounts, such as a 401(k) or 403(b), can be game-changers for your retirement savings. It's essentially free money. Employers provide matching contributions to your account, based on your own contributions, like a portion of your salary or bonuses.

These matches are offered to attract and retain employees and promote retirement savings. In some cases, employers also make nonmatching contributions, further boosting your retirement funds. In fact, more than 85% of 401(k) plans with Fidelity offer some form of employer contribution. Don't miss out on this opportunity to supercharge your retirement savings.

The typical 401(k) match at Fidelity follows this pattern: a dollar-for-dollar match on the first 3% of your salary and 50 cents on the dollar for the next 2%. If an employee contributes 5% of their income, the employer effectively adds 4% (3% + 1%, or half of 2% = 4%).

Notably, not all employees maximize their matches. Here's the average employer contribution per employee, including nonmatching contributions, based on age:

- 20–29: 4.0%

- 30–39: 4.6%

- 40–49: 5.0%

- 50–59: 5.2%

- 60–69: 5.2%

- 70+: 4.7%

- Overall average: 4.8%

Diversify Your Portfolio

To secure your retirement, diversify your investments across various assets. Consider reputable institutions like Vanguard, T. Rowe Price, Charles Schwab, Fidelity, and Prudential for a range of investment options.

Diversification spreads risk, offering a balanced approach that mitigates the impact of market fluctuations and maximizes potential returns, ensuring your retirement savings remain robust and resilient.

Wrapping It Up: Tips for Staying on Track

As you journey towards a secure retirement, keep these tips in mind:

- Consistency is key. Regular contributions, even if small, can yield significant results over time.

- Embrace employer matches. It's free money for your retirement.

- Diversify your portfolio to reduce risk.

- Keep an eye on income, and align your savings with your current lifestyle.

- Watch your personal spending. If it exceeds 30% of your income, the chances are that you don’t have enough left over for an adequate savings contribution.

- Start early and leverage the power of compounding.

- Adjust your strategy as you age, following key milestones.

By following these guidelines, you can navigate the path to retirement with confidence and financial security.

-balance-by-age.webp?w=1000&h=649&auto=format&fit=crop)

Conclusion

The landscape of retirement is constantly evolving. Staying informed and proactive about your finances is crucial. As we've explored, planning, saving, and investing wisely are the cornerstones of a secure retirement.

Remember what Warren Buffett, a renowned investor, once said: "It's not about timing the market, but time IN the market." Regularly reviewing your portfolio, keeping an eye on market trends, and adjusting your strategy accordingly will help you stay on track.

To receive more insightful financial tips, follow the Cash Store blog. Your financial future is in your hands, and we want to help you make the most of it.

FAQs

What is the recommended retirement savings by age 40?

By age 40, financial experts recommend having about three times your annual salary saved for retirement. This financial milestone sets you on a solid path to ensure your financial well-being during your golden years. Remember, it's never too late to start saving, and diligent planning can help you reach your goals.

How do 401(k) and IRA contributions impact average retirement savings?

401(k) and IRA contributions significantly impact average retirement savings. Regular contributions to these accounts over time can substantially boost your nest egg. Both accounts offer tax advantages that can further enhance your savings. The consistent commitment to funding these accounts can result in substantial growth and financial security for your retirement years.

How can I catch up if I'm behind on my retirement savings goals?

If you're behind on your retirement savings, there are ways to catch up. Start by saving an additional 1%, automate contributions, and redirect raises or windfalls to your retirement accounts.

Reducing unnecessary expenses and exploring a side hustle can provide extra income. These strategies, coupled with consistency, can help bridge the gap and improve your retirement outlook.

What are the main factors affecting retirement savings by age?

The main factors affecting retirement savings by age include income levels, investment choices, employer contributions, and personal financial habits. Income growth over time impacts savings potential.

Wise investment choices can optimize returns. Employer contributions and matches provide a significant boost. Additionally, personal financial discipline and life circumstances play a vital role in shaping retirement savings.

The content on this page provides general consumer information or tips. It is not financial advice or guidance. Each person’s circumstances are unique. The Cash Store may update this information periodically. This information may also include links or references to third-party resources or content. We do not endorse the third-party or guarantee the accuracy of this third-party information. There may be other resources that also serve your needs.

More Articles

What to Know About Crypto-Backed Loans

Curious about using your crypto as collateral? Discover how crypto-backed loans work, their benefits, risks, and what to consider before borrowing.

Read More >How Does Installment Loan Approval Work?

Curious about how installment loan approval works? Learn about the key factors lenders consider, the application process, and tips to improve your chances of approval.

Read More >Is it Better to Get an Installment Loan or Line of Credit?

Installment loan or line of credit—which is right for you? Learn the key differences, pros and cons, and how to choose the best option for your financial needs.

Read More >

Loan Amount is subject to loan approval. Loan terms and availability may vary by location. Approval rate based on complete applications received across all Cash Store locations. Customers can typically expect to receive loan proceeds in less than 20 minutes; however, processing times may vary. Loans / Advances are provided based on approved credit. Each applicant for credit is evaluated for creditworthiness.

Please see the Licenses and Rates page for additional product details.

Cash Store offers consumer credit products that are generally short-term in nature and not intended for long-term borrowing needs.

In Texas, Cash Store is a Credit Services Organization. Loans are provided by a non-affiliated third-party lender. Please see the Licenses and Rates page for links to Consumer Disclosures and choose the one for the product and amount that most closely relates to your loan request.

Customer Portal residency restrictions apply. Availability of funds may vary by financial institution.