Does Your Credit Score Need a Boost? Check Out These Tips from Cash Store

If you have ever signed up for a loan, borrowed money from a bank, or even opened up a checking account, the chances are that you have a credit score. Your credit score falls between 300 and 850, and the average American today has a credit score of 714, falling neatly within the good range. Generally, any score over 670 is considered good to excellent, but lenders often look for scores of 700 or higher. So why is that credit score so important? And what do you do if it falls below the good range? Check out our helpful tips to achieve credit score improvement.

Wondering How to Boost Your Credit Score?

Your credit score is far more important than many people realize. A good to excellent credit score can help you get the best interest rates and flexible borrowing terms. But sometimes, our credit scores fall lower than we want. Thankfully, there are some things you can do to boost your credit score fast.

Understanding Credit Scores

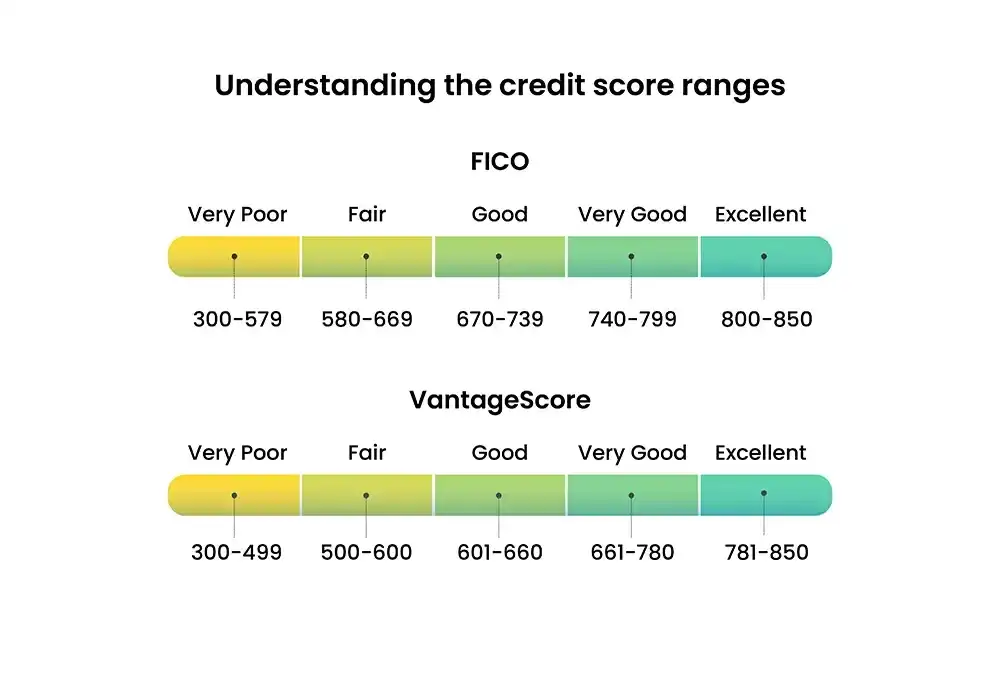

Let’s start by level-setting on just what the credit score ranges are and what goes into calculating your credit score in the first place. The most common version of your credit score is the FICO score, originally created in 1989 to provide a standard approach to reviewing a borrower’s credit and making lending decisions.

As we said earlier, your score falls from 300 to 850. The specific credit score ranges are as follows:

- Exceptional (800 to 850)—Borrowers falling within this range are considered low-risk, making it easier to secure loans than those with lower scores.

- Very Good (740 to 799)—Individuals with scores in this range have a history of positive credit behavior, increasing their chances of being approved for additional credit.

- Good (670 to 739)—Lenders generally view borrowers with scores of 670 and above as acceptable or lower-risk.

- Fair (580 to 669)—Individuals in this category, often labeled as "subprime" borrowers, may face higher-risk assessments by lenders, making it challenging to qualify for new credit.

- Poor (300 to 579)—Those with scores in this range often struggle to gain approval for new credit and need to seek loans for bad credit borrowers. If you find yourself in the poor category, improving your credit score is crucial before seeking new credit opportunities.

FICO scores are determined by analyzing various credit data in your credit report. These data points are categorized by five main factors: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), and credit mix (10%).

Reviewing Your Credit Report

The Fair Credit Reporting Act (FCRA) was enacted in 1970 to promote the accuracy, fairness, and privacy of personal information assembled by Credit Reporting Agencies (CRAs). As part of this act, individuals can gain access to their credit reports once per year at no charge.

The easiest way to access your credit report is via the Annual Credit Report website or one of the bureaus: Experian, Equifax, or TransUnion. When checking your credit report through one of the bureaus, you can sign up for a monitoring service that can inform you when your score goes up or down significantly.

Checking your credit report at least once yearly is a good way to ensure accuracy. If you find something wrong, you can file a dispute to correct your report as quickly as possible. Typical credit report errors include:

- Inaccurate information about your identity

- Incorrect reporting of account status

- Data management errors

- Balance errors

Establishing a Strong Foundation for Credit

Building a strong foundation and achieving a good or better credit score starts with mastering your finances, creating a budget that you can live with, and making smart borrowing decisions. And don’t be dismayed if you are just starting out and trying to build credit from scratch. You might not get approved the first time you apply.

For this reason, considering one of the following options is a good way to help you build credit and establish a score you can be proud of.

- Ask to be added as an authorized user on someone else’s account

- Apply for a secured credit card that leverages a cash deposit equal to your credit limit to be made when you open the account.

- Apply for a credit-builder loan that lets you borrow a small amount to demonstrate good borrowing behaviors. You make regular, on-time payments that help you establish a credit history.

- If you are approved for a traditional credit card or personal loan, make sure you make at least your minimum-required payments on time every month. Missing a payment and not making it up within 30 days can cause your credit score to plummet by as much as 180 points.

- Pay attention to your credit utilization and keep it at 30% or below. This means that if you have a credit line of $10,000, you should always keep your balance at $3,000 or less. We’ll explore this a bit further in the next section.

Managing Credit Utilization

Many borrowers don’t realize that just because they are approved for a specific amount doesn’t mean they should borrow up to that amount. This is especially the case with credit cards. For example, let’s say you have two or three credit cards, each with a credit limit of $5,000. Take steps to keep those balances at $1,500 or less. This figure represents your credit utilization ratio which accounts for 30% of your overall credit score - so keeping those balances at 30% or less of your available credit is important.

But managing your credit utilization is about more than just working to stay under that 30% goal to protect or improve your credit score. It is also important to consider that the more you spend on your credit cards each month, the higher your monthly payment will be. The higher your monthly payment, the more challenging it can be to make all of your other monthly payments on time. This leads us to the importance of paying your bills on time.

Paying Bills on Time

As we mentioned earlier, a failure to make a monthly payment can have some serious consequences to your credit score. The fact is that your payment history is the single most important factor that goes into your score, representing 35% of the calculation. This means that you must make at least the minimum monthly payment on time each month. If you are struggling to make those payments, it’s a big indicator that it’s time to go back to that budget to reassess how much you spend each month on your wants vs. your needs. You may find that you will have to change your spending habits.

Diversifying Your Credit Mix

Diversifying your credit mix means you shouldn’t put all your eggs in one basket. So, avoid more than two or three credit cards to have a healthy credit mix. Seek for a mix that includes a mortgage or rent payment, an auto loan (if you have a car), no more than three credit cards, and a student loan or other personal loan. Though your credit mix only represents 10% of your credit score, it’s important to remember that keeping a healthy mix can also make managing all of those monthly expenses more manageable. Too many credit cards, for example, is a fast way to drive up your debt.

Handling Existing Debts

At this point, we’ve probably hammered home the notion that you must make your payments on time every month, but it’s also important to consider how much you pay towards those debts monthly. Paying only the minimum, while it helps protect your payment history, doesn’t necessarily help pay down your debt fast.

For example, the next time you get a credit card statement, take a look at the payment history section. All credit card statements are required to provide some critical information. One of those data points will tell you how much you will pay over a period of time if you only pay the minimum payment. It will also show how much you can save if you increase your monthly payment. If you have the means to pay more than your minimum monthly payment, it can benefit you to do so. Not only does this help your payment history, but it also helps with your credit utilization as it effectively drives down your balances.

Avoiding Credit Mistakes

New credit represents 10% of your credit score. This is looking at how often you apply for credit. Applying for too many types of credit in a short period of time isn’t a good thing and can harm your credit score. As a rule of thumb, waiting at least 90 days, and up to six months between applying for credit if possible is good guidance.

So if you apply for a new credit card in January, wait until July or July to apply again. And if you were declined for that first card, take steps in those months while you wait to improve your credit score. Your credit score goes up and down regularly as your creditors report new information. So taking steps to drive down your debt during those six months, and paying your bills on time, may very likely result in a higher score.

Monitoring Progress and Demonstrating Patience

When building and improving your credit, part of the strategy requires patience. While your credit score goes up and down regularly, it may take some time to see noticeable changes. Remember that you can generally expect your credit score to update at least once a month. So if you are trying to make some improvements, give it time. After a couple of months, you should hopefully see your score going in the desired direction.

Boost Your Credit Score for Better Creditworthiness

If you're looking to boost your credit score, these valuable tips from Cash Store can help. By effectively managing existing debts, you can demonstrate responsible financial behavior and improve your creditworthiness. Additionally, regularly monitoring your credit progress and implementing credit-building strategies can set you on a stronger credit profile. Take control of your credit and pave the way for a brighter financial future.

*The content on this page provides general consumer information or tips. It is not financial advice or guidance. Each person’s circumstances are unique. The Cash Store may update this information periodically. This information may also include links or references to third-party resources or content. We do not endorse the third-party or guarantee the accuracy of this third-party information. There may be other resources that also serve your needs.

More Articles

What to Know About Crypto-Backed Loans

Curious about using your crypto as collateral? Discover how crypto-backed loans work, their benefits, risks, and what to consider before borrowing.

Read More >How Does Installment Loan Approval Work?

Curious about how installment loan approval works? Learn about the key factors lenders consider, the application process, and tips to improve your chances of approval.

Read More >Is it Better to Get an Installment Loan or Line of Credit?

Installment loan or line of credit—which is right for you? Learn the key differences, pros and cons, and how to choose the best option for your financial needs.

Read More >

Loan Amount is subject to loan approval. Loan terms and availability may vary by location. Approval rate based on complete applications received across all Cash Store locations. Customers can typically expect to receive loan proceeds in less than 20 minutes; however, processing times may vary. Loans / Advances are provided based on approved credit. Each applicant for credit is evaluated for creditworthiness.

Please see the Licenses and Rates page for additional product details.

Cash Store offers consumer credit products that are generally short-term in nature and not intended for long-term borrowing needs.

In Texas, Cash Store is a Credit Services Organization. Loans are provided by a non-affiliated third-party lender. Please see the Licenses and Rates page for links to Consumer Disclosures and choose the one for the product and amount that most closely relates to your loan request.

Customer Portal residency restrictions apply. Availability of funds may vary by financial institution.